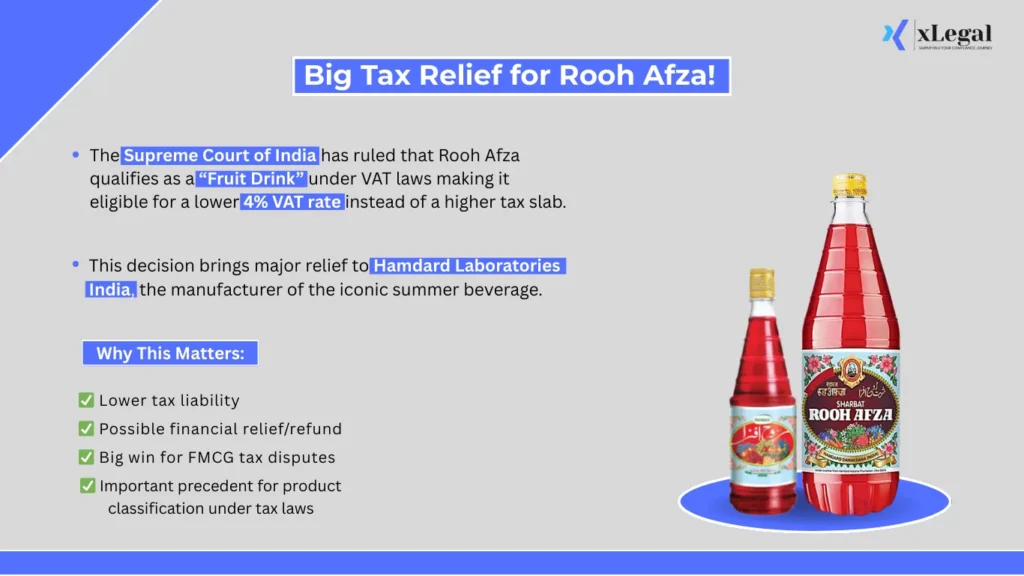

In a major ruling that will have far-reaching implications for the indirect tax jurisprudence landscape, the Supreme Court of India has held that Rooh Afza is a “fruit drink” under the applicable VAT laws. This means that the popular drink is liable to be taxed at a concessional rate of 4% VAT, as opposed to a higher rate of taxation….